The 2026 Emergency Fund: Why 3 Months is No Longer Enough

The financial rulebook has been rewritten. While "3 months of expenses" was the standard advice for decades, the 2026 landscape—marked by rapid AI-driven job shifts and high medical inflation—has made 6 months the new "Survival Minimum."

An emergency fund isn't an investment meant to make you rich; it’s a shield meant to keep you from liquidating your long-term wealth when life hits hard.

Step 1: Defining Your "True" Survival Expenses

Most people underestimate their target because they only think about rent and food. To build a bulletproof fund, you must account for every "Must-Pay" obligation.

- The Checklist: * Rent or Home Loan EMIs.

- Utility bills (Electricity, Water, 5G/Fiber).

- Insurance Premiums (Life, Health, Vehicle).

- Essential Groceries and Medicine.

- Children’s School Fees.

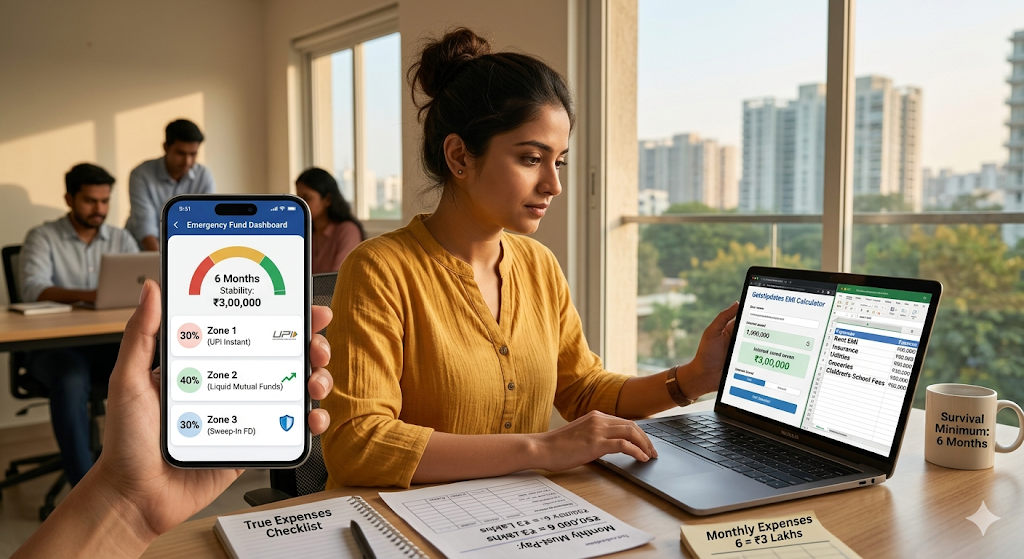

- The Math: If your "Must-Pay" total is ₹50,000, your 2026 target is ₹3,00,000 (6 months). If you are a freelancer or business owner, experts now recommend pushing this to 9–12 months.

Step 2: The Liquidity vs. Returns Trade-off

The biggest mistake you can make is "investing" your emergency fund in the stock market. If the economy crashes and you lose your job, the market will likely be down too—forcing you to sell your assets at a massive loss.

The 2026 Strategy: Focus on 100% Liquidity over high returns. You need to be able to access this money within 24 hours.

[Image showing a split between a mobile banking app for instant cash and a liquid fund dashboard for safety]

Step 3: Asset Allocation for Safety

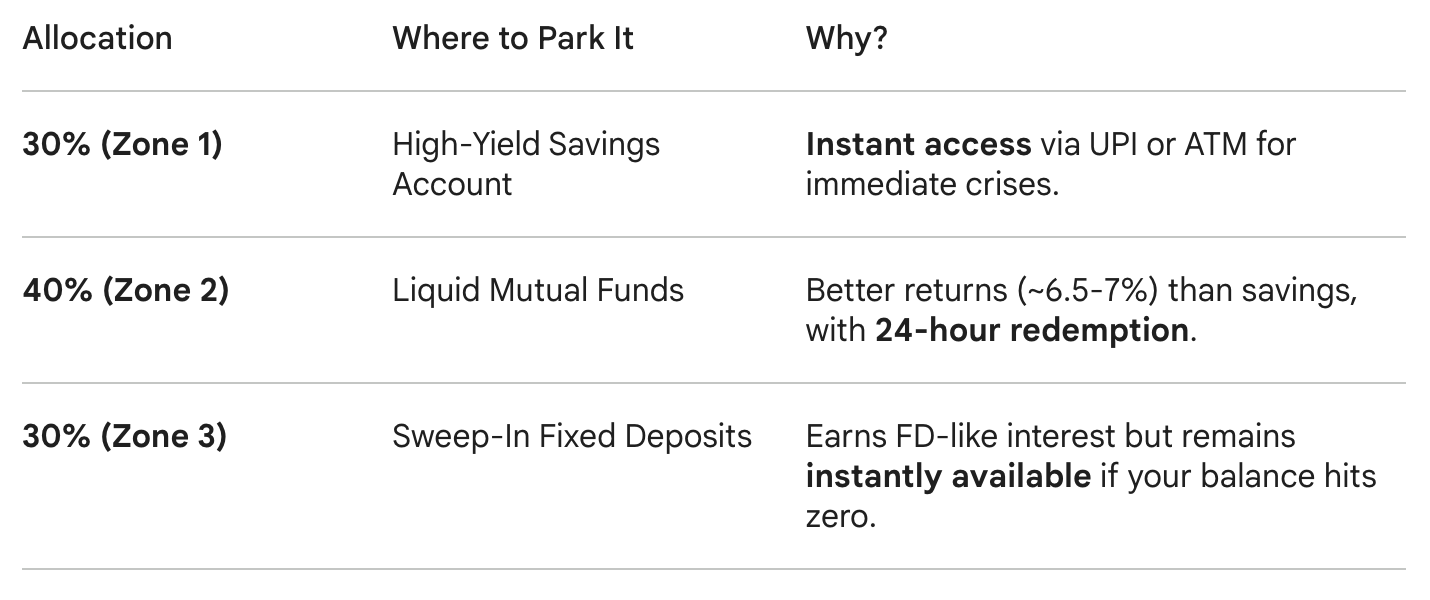

In 2026, the ideal way to park your fund is to split it across different "access zones" to balance speed and inflation protection.

Earns FD-like interest but remains instantly available if your balance hits zero.

Pro Tip: Don't wait until you have the full amount to start. Use an EMI Calculator to see how much "interest-heavy" debt you can avoid by having even a 1-month buffer. Treat your monthly contribution to this fund as a non-negotiable bill.