The Shift in Bill Payment Rewards

In 2026, the landscape of credit card bill payments has matured. The days of random "scratch cards" with ₹1 cashback are largely over. Today, savvy "Transactors"—users who pay their full statement balance every month—are leveraging a sophisticated ecosystem of third-party aggregators and official bank portals to extract significant value from their bill payments. If you are simply paying your bill via a standard bank transfer, you are leaving money on the table.

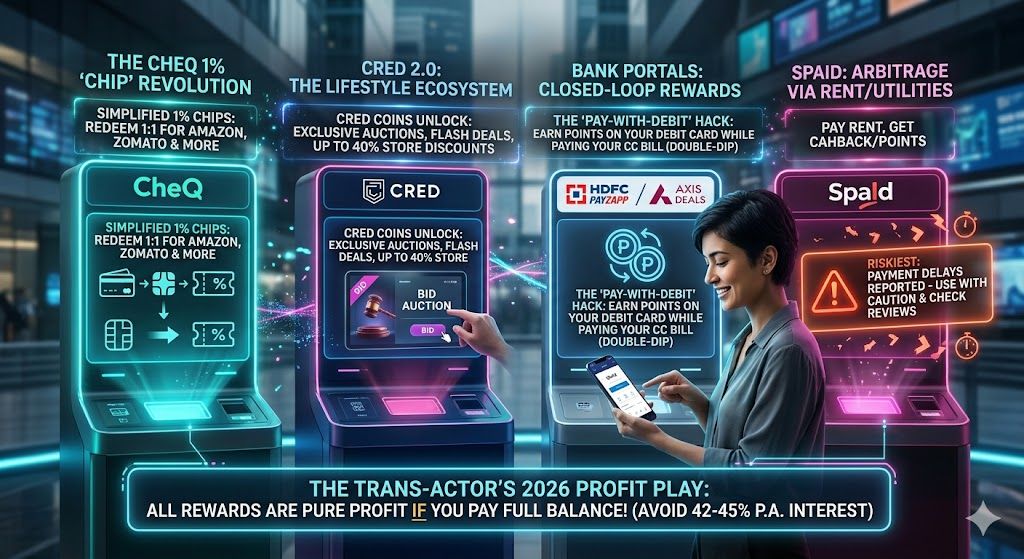

CheQ and the 1% 'Chip' Revolution

CheQ has emerged as a dominant player in 2026 by simplifying the reward structure. By paying your credit card bills through the CheQ app, you earn CheQ Chips equivalent to 1% of your payment value (capped at ₹4,000 per month for premium users). These chips are not just digital vanity metrics; they can be converted into gift vouchers for popular brands like Amazon, Zomato, and Tata CLiQ at a 1:1 ratio. For someone with a monthly bill of ₹50,000, this translates to a steady ₹500 in monthly savings just for paying what they owe.

CRED in 2026: The Ecosystem Play

CRED continues to be the choice for high-CIBIL individuals, but its strategy has shifted. Instead of direct cashback, CRED now focuses on its "Member-Only Auctions" and CRED Flash. By paying your bills on CRED, you earn CRED Coins which can be used to unlock massive discounts on high-end lifestyle products and travel packages. In 2026, the real value in CRED lies in the "Kill the Bill" jackpots and the exclusive access it provides to the CRED Store, where coins can often offset up to 40% of the product cost.

Leveraging Bank Portals: PayZapp and Grab Deals

Official bank apps like HDFC PayZapp and Axis Bank's Grab Deals have introduced "Closed-Loop Rewards." When you pay your HDFC credit card bill using PayZapp (linked to a HDFC Debit Card), you can often earn Reward Points on your debit card that were previously reserved for merchant spends. This "double-dipping" strategy—earning rewards while paying off the debt that earned you rewards in the first place—is the ultimate 2026 hack for maximizing the ROI on your plastic.

The Rise of UPI on Credit (RuPay)

The integration of RuPay credit cards with UPI has changed the game for small-ticket payments. While traditional bill payment rewards focus on the "settlement," RuPay UPI focuses on the "spend." By using a RuPay credit card for your daily tea, groceries, and local QR payments, you accumulate points on transactions that were previously cash-only. Paying these small, frequent bills via an aggregator then layers a second level of rewards on top of those merchant-earned points.

The "Transactor" vs. "Revolver" Math

All these rewards are predicated on one absolute rule: You must be a Transactor. If you carry a balance and pay only the "Minimum Amount Due," the interest rates (which have climbed to 42-45% per annum in 2026) will instantly dwarf any reward you earn. A ₹500 reward from CheQ is meaningless if you are paying ₹2,000 in monthly interest. Treat your credit card as a payment tool, not a loan, and always pay the "Total Amount Due" to ensure your rewards remain pure profit.