Home Loan Prepayment vs. Mutual Funds in India: The 2026 Guide to Smart Investing

For many homeowners in India, a common and critical financial question arises:

Should I prepay my home loan, or invest my extra savings every month?

The right answer isn't universal; it hinges on three key factors:

- Your loan's interest rate.

- Your expected investment returns.

- Your personal comfort with risk.

To give you a clear and practical understanding, let's explore this dilemma with a realistic example scenario.

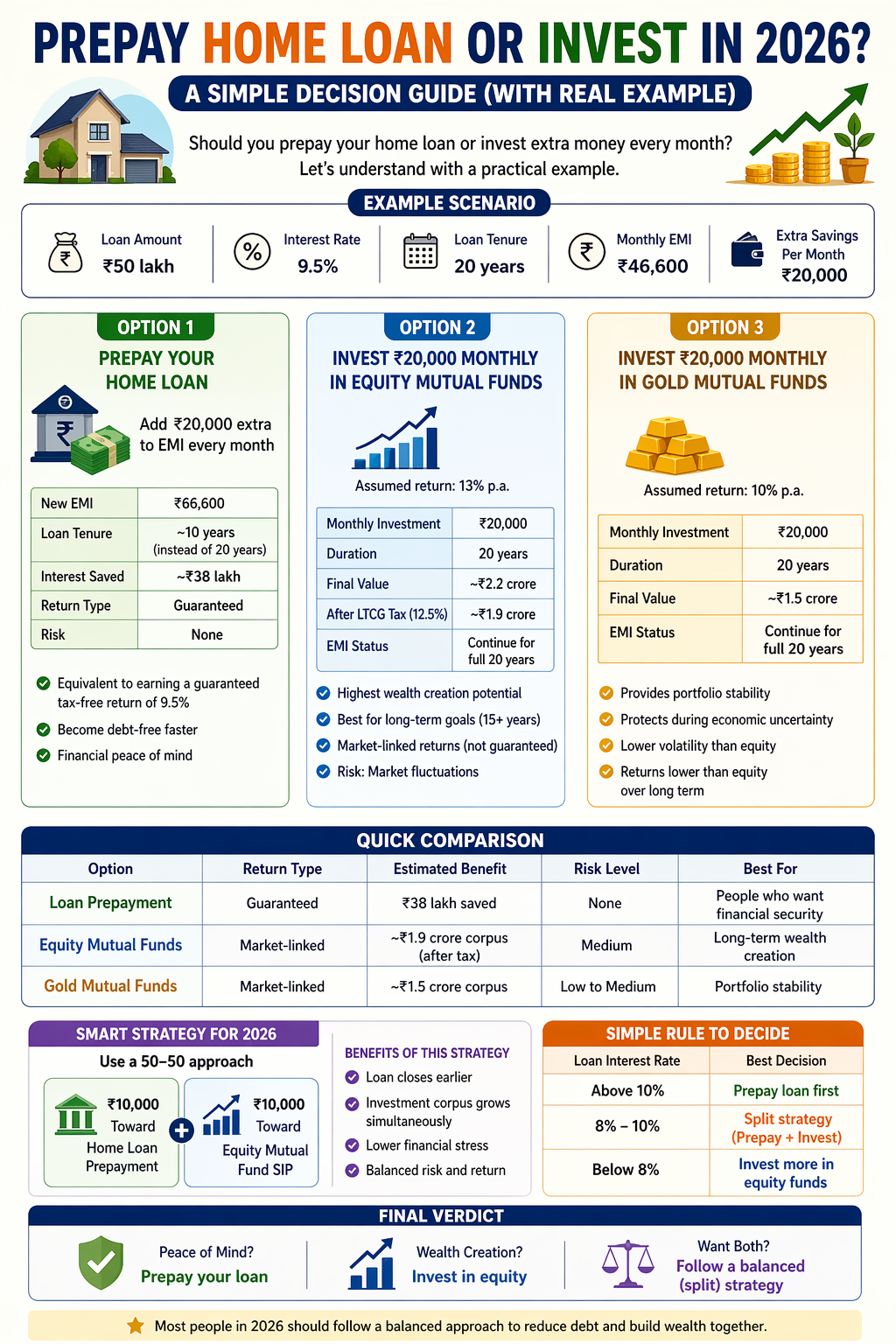

Example Scenario: The ₹50 Lakh Dilemma

Let's assume you have the following finances:

- Loan Amount: ₹50 Lakh

- Interest Rate: 9.5%

- Loan Tenure: 20 Years

- Monthly EMI: ₹46,600

- Extra Monthly Savings: ₹20,000

You now have a crucial choice to make with that extra ₹20,000:

- Prepay the Loan: Increase your EMI and become debt-free sooner.

- Invest in Equity Mutual Funds: Aim for higher growth through stock markets.

- Invest in Gold Mutual Funds: Seek stability with a traditional safe-haven.

Let’s dive deep into each option.

Option 1: The Power of Home Loan Prepayment

What happens if you use that extra ₹20,000 to increase your monthly payment?

- New Monthly Payment: ₹66,600

- Tenure Reduction: Your loan is paid off in approximately 10 years, down from 20.

- Total Interest Saved: You avoid paying a staggering ~₹38 Lakh in interest.

Why This is a Great Strategy

Choosing prepayment is equivalent to earning a guaranteed, tax-free return of 9.5%. This is because every rupee you prepay saves you the interest you would have otherwise paid to the bank.

Benefits:

- Guaranteed Return: You know exactly how much you're saving.

- Zero Market Risk: Unaffected by stock market ups and downs.

- Debt-Free Faster: The psychological relief of owning your home sooner is significant.

- Peace of Mind: Provides unparalleled financial security.

Option 2: The Wealth Creation Potential of Equity Mutual Funds

What if you invest that ₹20,000 monthly instead, continuing your original EMI for the full 20 years?

- Assumption: We'll use an expected annual return of 13%.

- The Power of Compounding: By investing ₹20,000/month for 20 years:

- Final Value: Approximately ₹2.2 Crore.

- After-Tax (LTCG) Corpus: Approximately ₹1.9 Crore.

Why This is a Great Strategy

Equity investing offers the highest potential for wealth creation, making it an excellent choice for long-term goals.

Benefits:

- Highest Wealth Potential: Offers the best chance to outpace inflation and build substantial wealth.

- Best for Long Horizons: Ideal for goals like retirement that are 15+ years away.

- Builds a Large Corpus: Creates a significant financial asset for your future.

Risks to Consider:

- Market Fluctuations: Value can go down in the short term.

- Returns Not Guaranteed: The 13% is an average and not a promise.

Option 3: The Stability of Gold Mutual Funds

Is the traditional safe-haven of gold the right choice for your extra savings?

- Assumption: We'll use an expected annual return of 10%.

- Investing Journey: By investing ₹20,000/month for 20 years:

- Final Value: Approximately ₹1.5 Crore.

Why This is a Great Strategy

Gold primarily acts as a hedge against inflation and economic uncertainty. It adds a layer of stability to your overall portfolio.

Benefits:

- Portfolio Stability: Offers a smooth-out effect when other assets are volatile.

- Crisis Protection: Often performs well during stock market crashes.

- Lower Volatility: Tends to have less extreme price swings than equities.

Limitations:

- Lower Long-Term Growth: Statistically, it underperforms equities over long periods.

- Returns Close to Loan Rate: The potential gain isn't significantly higher than the interest you're paying on your loan.

The Quick Comparison: Which Path is for You?

The Smart Strategy for 2026: The "Balanced Approach"

Instead of an "all or nothing" choice, the most practical strategy for most Indian households in 2026 is a split strategy.

For example, split your ₹20,000 extra savings:

- ₹10,000: Towards home loan prepayment.

- ₹10,000: Towards an Equity Mutual Fund SIP.

Why This Balanced Strategy Works

- Hybrid Benefits: You close your loan earlier than scheduled and build an investment corpus at the same time.

- Reduced Stress: You're actively reducing debt while also planning for the future.

- Optimized Returns: You get a balance of a guaranteed return and the potential for higher market returns.

The Simple Rule to Help You Decide

Here's a quick rule of thumb to guide your decision based on your interest rate:

- If Loan Interest is > 10%: Prioritize loan prepayment. The guaranteed return is hard to beat.

- If Loan Interest is 8-10%: A split strategy is typically the most effective and balanced choice.

- If Loan Interest is < 8%: Investing in equity mutual funds is often the best path for long-term wealth creation.

The Final Verdict

The "right" answer comes down to your priorities:

- Choose Prepayment if your primary goal is the peace of mind that comes with being debt-free.

- Choose Equity Investing if your primary goal is maximizing wealth creation.

- Choose a Split Strategy if you want the best of both worlds: financial stability and long-term growth.

In the current financial landscape of 2026, a balanced approach stands out as the most sensible strategy for achieving true financial wellness.