Cracking the Credit Code: Secured vs. Unsecured Credit Cards in 2026

If you’re staring at a "Thin File"—the industry term for having little to no credit history—scoring a standard credit card can feel like trying to get into an exclusive club without an invite. In the 2026 financial landscape, understanding the "Gatekeepers" of credit is the fastest way to build a high-performance score.

Whether you're a Gen-Z professional starting out or someone looking to rebuild, here is how to choose your bridge to financial freedom.

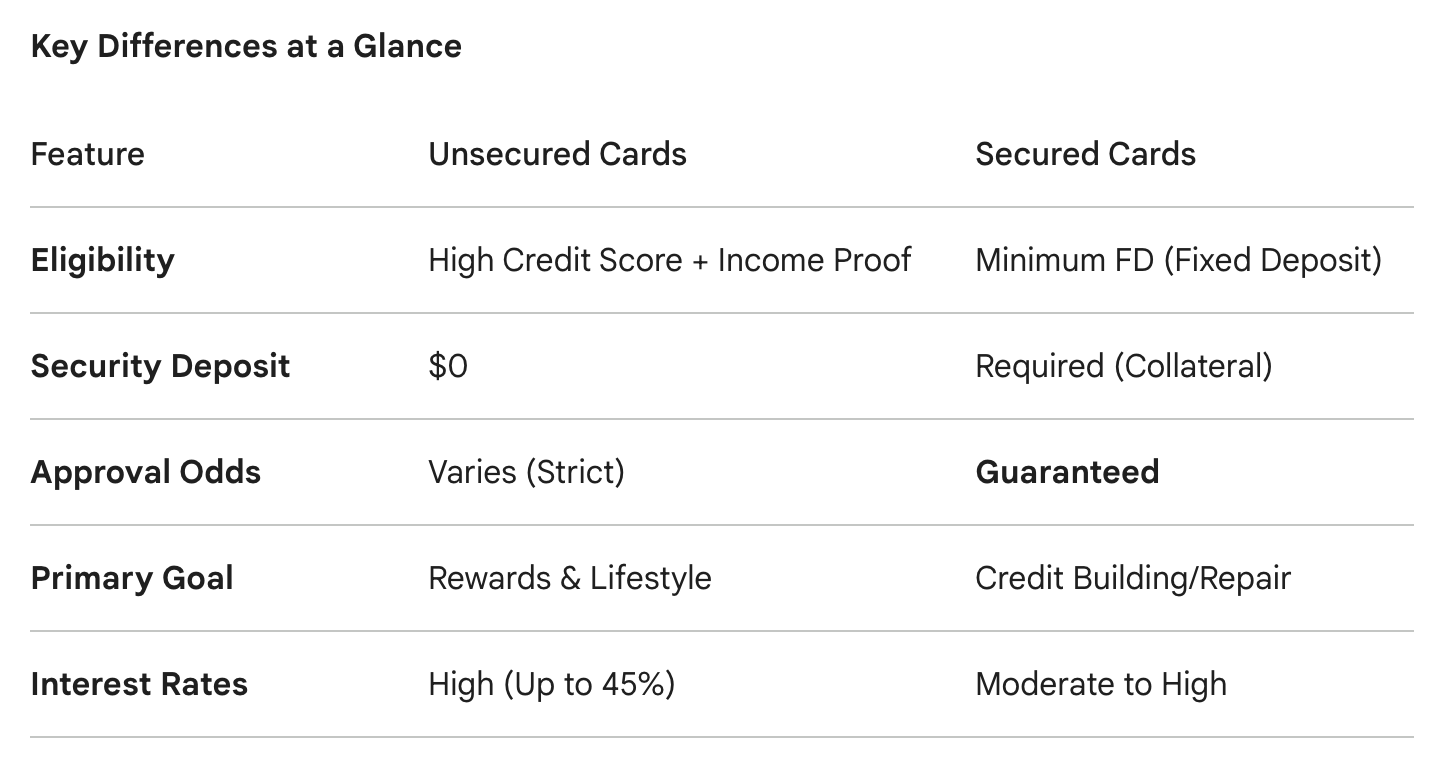

1. Unsecured Cards: The High-Stakes Reward Kings

Most flashy cards you see on social media are unsecured. These are issued based on your reputation (credit score) and your paycheck.

- The Perks: These are the "Flex" cards. We’re talking premium lounge access, 5% cashback on trending apps, and high credit limits that scale with your income.

- The Catch: Because the bank is taking a risk on you, the barrier to entry is high.

- The Risk: If you don't pay in full, the "convenience" gets expensive. Interest rates in 2026 typically hover between 36% and 45% p.a., making disciplined repayment a non-negotiable.

2. Secured Cards: The "Guaranteed" Credit Builders

Secured cards are the ultimate life hack for those the traditional system ignores. These are backed by a Fixed Deposit (FD), which acts as collateral.

- Guaranteed Approval: Since the bank has your FD as a safety net, they don't care about your past credit mistakes or lack of history.

- The 2026 Trend: Fintechs have revolutionized this space. Most now offer zero annual fees and "instant virtual issuance," allowing you to start building credit within minutes of opening an FD.

- Credit Limit: Usually, your limit is set at 80–90% of your deposit amount.

Pro Tip: Treat your secured card like a training gym. Use it for small, recurring subscriptions, pay it off instantly, and watch your "Thin File" transform into a Prime Score in as little as 6 to 12 months.